The SEC's approval of the first US Bitcoin Futures ETF marks a monumental shift in institutional and regulatory attitudes towards crypto.

In just two days, ProShares' Bitcoin ETF topped $1 Billion in assets. Approximately 10% of all Bitcoin ($125 Billion) is now held in corporate treasuries. And 52% of institutional investors already report having exposure to crypto (Fidelity Survey)

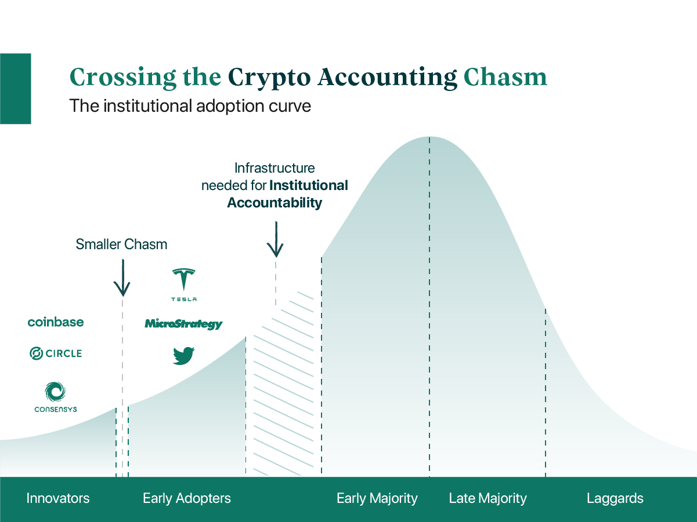

The debate about whether institutions are going to adopt crypto is over. The industry has crossed the chasm from the early adopters to the early majority.

In this article, we're taking a deep dive into the types of institutions adopting crypto, the challenges they face, and the regulatory and technical infrastructure they are demanding from the industry.

Where are we in the institutional adoption curve?

Geoffrey Moores, technology adoption lifecycle serves as a useful model for charting the adoption of crypto.

For those unfamiliar with the model, it is based on the classic bell curve distribution. It helps us visualize the adoption of new technologies over time: starting with a small handful of early adopters, moving through the massive mid-market, to eventually find its way into the hands of even the most change-resistant consumers.

For the crypto industry, it is helpful to think of these segments in terms of the examples below:

- Innovators (2%): Consensys, Coinbase, Circle, Layer 1 & 2 Projects

In the 11 years since the first Bitcoin transaction, a $2.7 trillion industry has emerged. Smart contract chains like Ethereum, Polkadot, Solana, now have over $200 Billion in value locked into their thriving DeFi and NFT ecosystems. An array of companies like Coinbase, Circle, and Consensys provide the foundations for this industry in the form of exchanges, trusted stablecoins, and digital wallet infrastructure.

Blockchain innovators are irreversibly changing the accepted ways of doing business across multiple industries. This rapidly growing segment may represent a small proportion of the industry as it stands today, but as user adoption grows the innovators become 'institutions' in their own right.

Web 2.0 businesses (eg. Facebook & Google) serve as pertinent examples of disruptive startups becoming institutions. The key difference with web 3.0 is the move to decentralized models. The 'institutional' influence of blockchain innovations is likely to be distributed across a spectrum of centralized and decentralized organizations, businesses, and users.

- Early Adopters (15%): Tesla, MicroStrategy, Twitter

Elon Musk, Jack Dorsey, and Michael Saylor represent the non-crypto native, early adopters. Taking BTC payments for cars, enabling tipping, and NFT creation on Twitter, and transforming a software intelligence company into a publicly traded vehicle for Bitcoin investing represent this segment of the distribution.

- Early Majority (34%): Hedge funds, Family Offices, Asset Managers, Corporate Treasuries.

The early majority are willing to gain exposure to this emerging technology and asset class, however, they need familiar financial vehicles and infrastructure such as ETFs, investment trusts, mutual funds that plug into their current investment workflows. They also need assurance around regulatory and tax implications of adoption.

This is where we are. The early majority is pouring in and is in need of key infrastructure to help bridge the chasm between the blockchain and their current financial workflow.

- Late Majority (34%): Sovereign Treasuries, Pension Funds, Endowment Funds

- Laggards(15%): Crypto Skeptics

Regulation will play a fundamental role in the rate of institutional adoption. Larger, more regulated entities have more onerous compliance and regulatory monitoring, reporting, and oversight. This is we saw strong early adoption by smaller funds and family offices. They are keen to take advantage of the exceptional investment returns and are also able to do so from a regulatory and compliance perspective.

Institutions & corporates: who are they and why are they adopting crypto?

Broadly speaking, there are two primary use cases for institutions and corporates holding crypto.

Investment & wealth preservation |

Payments & operations |

| Crypto Hedge Funds | Crypto-native businesses |

| Traditional Hedge Funds | FinTech |

| Family Offices | Gaming, Art & Collectible Creators |

| Pensions & Endowments | Traditional companies |

| Corporate Treasuries | Tax and Revenue Authorities |

| Sovereign Treasuries |

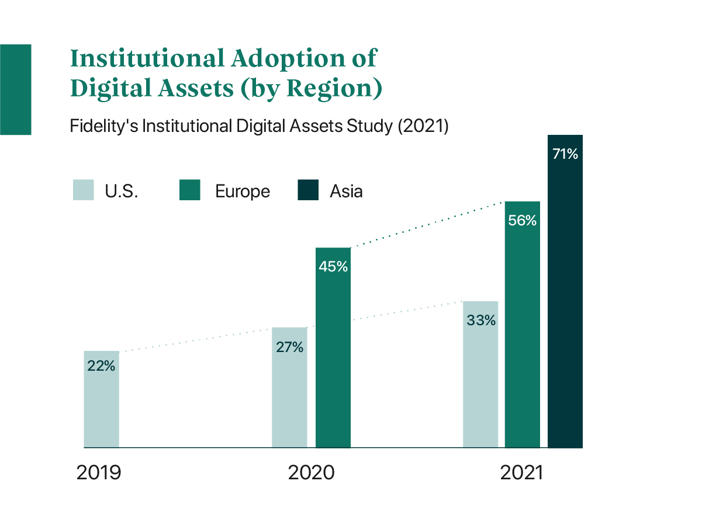

On the investment side, native crypto hedge funds (HF) and venture capital (VC) funds have the highest adoption levels. Followed by traditional hedge funds, family offices, corporate treasuries, and finally pension and endowment funds. (Fidelity Report, Sept 21)

We also see interesting trends across different regions. Institutional actors in Asia are most comfortable with digital assets, followed by Europe and finally the US. However, it is fair to assume the US adoption was restricted by the lack of regulated financial vehicles available. With the recent approval of ETFs, it is fair to assume adoption will grow rapidly.

On the payments and operations side, businesses such as Starbucks and Microsoft are now taking payments in crypto. Crypto-native businesses such as Binance are also choosing to pay their employees in crypto. And most substantially, El Salvador made Bitcoin legal tender. This adoption is made possible by an ecosystem of businesses providing payments and custody infrastructure, such as Request Network, Bakkt, and Fireblocks.

Top concerns for corporates and institutions

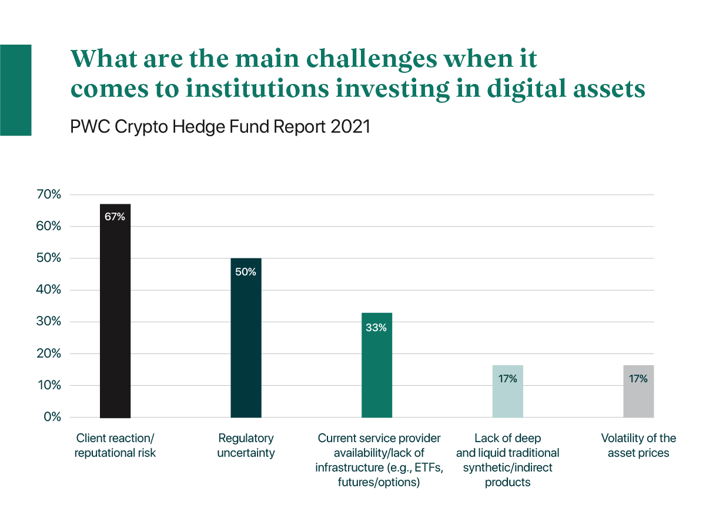

As per PWC's 2021 study, The top three challenges cited by hedge fund managers who currently invest in digital assets are:

- Client reaction & reputational risk

- Regulatory uncertainty

- Current service provider availability/ lack of infrastructure

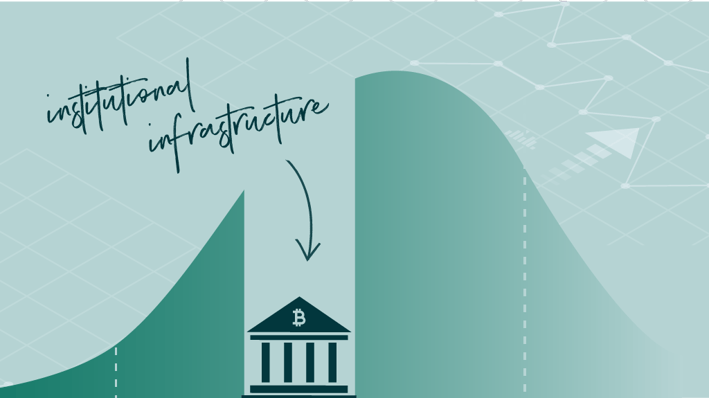

Accounting and reporting infrastructure is crucial for the next stage of digital adoption, as it helps the funds build trust with clients. Accountability is essential in an industry that appears shrouded in uncertainty to the average investor.

At this stage of hyper-adoption, institutions and financial service providers are seeking out infrastructure solutions to help them better navigate the crypto space. The three pillars of institutional infrastructure are:

- Security: Custody of crypto assets

- Payments: Efficient and cost-effective ways of transacting with their assets

- Accounting: Tracking crypto activity and reporting for tax and audit

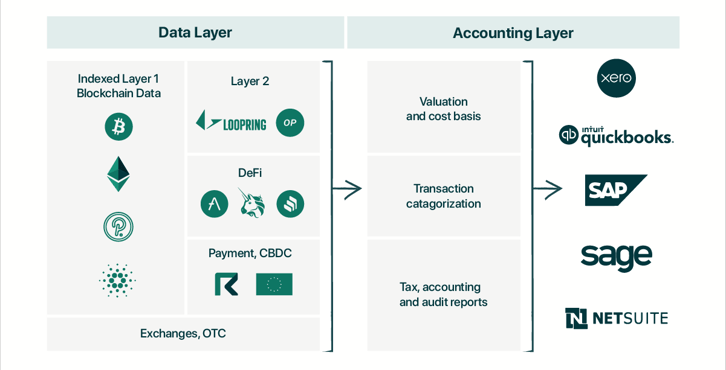

At Cryptio, we're building this essential back-office infrastructure. Bridging the gap between the blockchain and accounting systems – transforming DeFi, custody, OTC, and exchange data into auditable records for accounting, treasury, and tax filings.

Learn more about how you can streamline your crypto accounting here.

The two-fold accounting problem: regulatory & technical

The taxation of the types of crypto and such income/gains derived will be jurisdiction-specific and, in many jurisdictions, the tax treatment is not yet clear. This is the regulatory accounting challenge.

Regulatory

Tax authorities are now beginning to engage with the tax implications of crypto assets. Different authorities may take different approaches and institutional stakeholders in the industry are keeping a close eye on these developments.

Financial institutions setting up new entities for their digital asset investments may consider many of the same tax issues are considered when structuring, and operating traditional hedge funds and family offices. But there are also new forms of transactions that have no equivalent counterpart in traditional finance.

These new transaction types are specific to blockchain and programmable money – for example, staking income, mining income, token rewards, coin lending, hard fork, chain split, and airdrops. The tax characterization of these events may evolve from initial acquisition throughout the holding period until disposal.

Many crypto-friendly jurisdictions have also emerged – both from a regulation and tax perspective. The most recent Chinese crackdown saw a mass exodus of bitcoin mining businesses and a large move to the US (now accounting for 35% of BTC's hash rate). This goes to show,

Jurisdiction-based regulation will not decide whether institutions adopt crypto – it will decide where crypto businesses and institutions set up their entities.

Many jurisdictions have already safe harbors in place to prevent traditional funds from paying tax in the location of the investment team as a means of encouraging the development of their local investment management industries. A similar model could emerge for crypto-based funds and institutions.

Technical

Over the last 15 years, finance teams and accounting firms have transferred their processes to accounting systems such as Xero, QuickBooks, and NetSuite. With a host of transactions now taking place on blockchains, institutions and corporates need to find ways to bridge the gap between their blockchain activity and their current accounting systems.

Growing interest across institutional segments underscores the need for a diverse set of products and solutions to meet investors where they are in their digital assets journey.

– Peter Jubber, Managing Director, Fidelity Digital Funds

Institutions and corporates using DeFi protocols like Uniswap, Sushiswap, 0X, Compound, Aave, have the additional challenge of identifying these smart contracts and recognizing the kind of transaction happening – signing, wrapping, depositing, withdrawing, and more.

The back-office infrastructure needed to identify and index needs to develop as the ecosystem grows. Accountants, auditors, and fund administrators will need to educate themselves on crypto taxation and improve their technical infrastructure. If they want to service this rapidly growing market, they’ll need to embrace technology that bridges the accounting chasm between the blockchain and their current systems.

About Cryptio

Cryptio's institutional-grade accounting software let you track your assets & transactions from DeFi protocols, wallets, exchanges, and institutional custodians to construct a complete picture of your digital asset activity. Transform blockchain data into auditable records for accounting, treasury, and tax filings.